BLOG POST 11 — Ask Uncle Alvin About Unique Real Estate and Stock Market Facts Overlooked By Investors

My kids have been asking and I do tell them to invest in index funds and to just leave it. For now, they each have homes of their own and the next step is to invest in the stock market. Real estate has increased a lot even with interest rates going up — is it better to invest more in real estate or stocks?

Your kids are doing great starting out as homeowners and now looking to invest in the stock market! Uncle Alvin wants to provide them and fellow nieces and nephews with unique real estate and stock market facts that may be helpful but are little-known and overlooked by most investors.

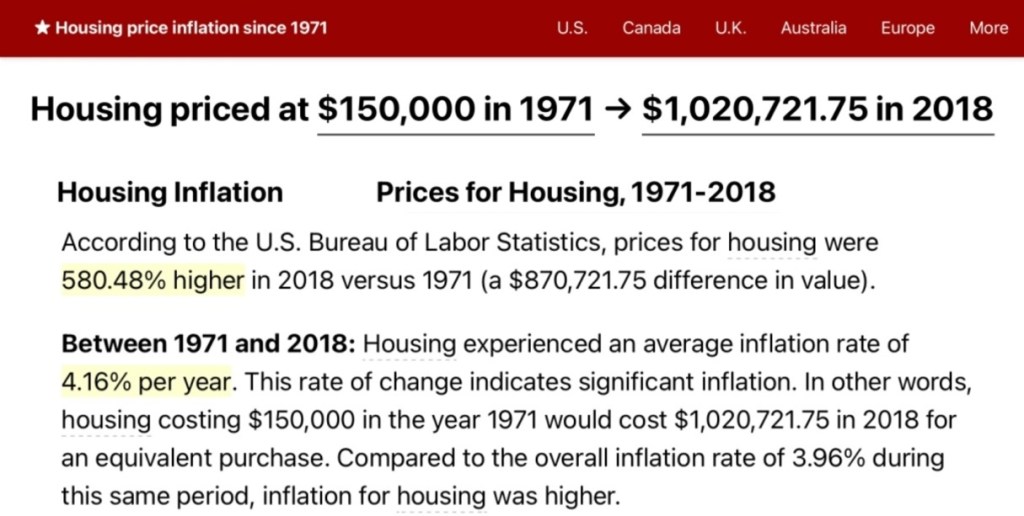

The first real estate fact is that Uncle Warren Buffett bought a Laguna Beach home in 1971 for $150,000 and sold the home 47 years later in 2018 for $7.5 million.

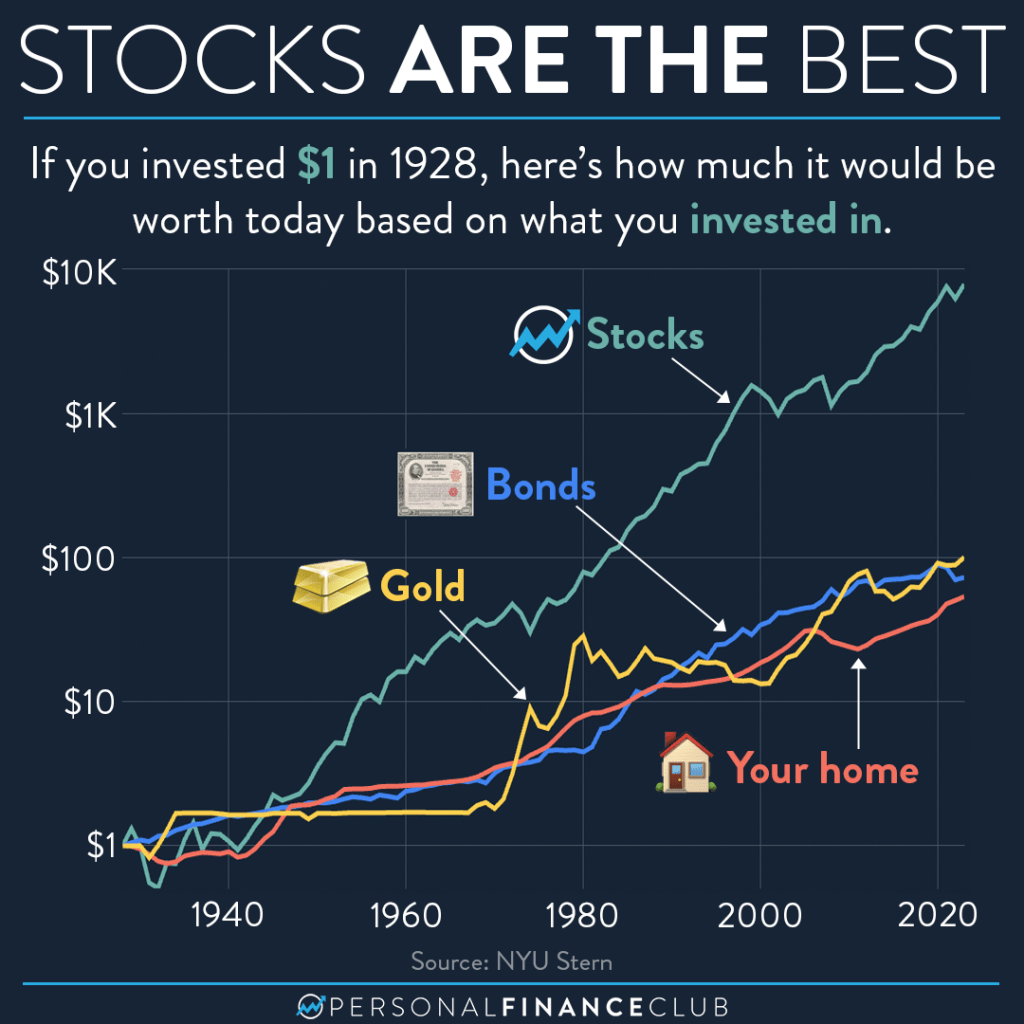

The second stock market fact is that an investor who bought an S&P 500 fund in 1971 with $150,000 could sell the fund 47 years later for $16.5 million.

These two facts overlooked by most investors show that a stock market investment in an ordinary index fund that any investor can buy, beats a real estate investment in one of the best locations in the world that very few investors can buy.

A key real estate fact overlooked by many investors is that only prime locations increase in value like Uncle Warren’s Laguna Beach home that appreciated after 47 years from $150,000 to $7.5 million. Most real estate properties are in non-prime locations that typically appreciate only slightly faster than inflation.

This means that $150,000 invested in real estate in most locations in 1971 that appreciated slightly faster than inflation would increase 47 years later to $1 million, less than Uncle Warren’s Laguna Beach home that increased to $7.5 million and much less than the S&P 500 index fund that increased to $16.5 million.

Unfortunately, very few people can afford to buy real estate in prime locations. Fortunately, anyone can buy S&P 500 index funds with expense ratios less than 0.05% and generate superior long-term returns from the stock market that significantly beat the long-term returns from real estate in nearly all locations, even prime locations like Uncle Warren’s Laguna Beach home.

Another real estate fact overlooked by investors is that real estate has high expenses in the form of property taxes, insurance, utilities, maintenance and repairs — and unfortunately the tyranny of compounding costs (see BLOG POST 2) makes real estate equivalent to high cost mutual funds that take away roughly 75% of the return over the long term and leave investors with only 25% of the return.

This means if $150,000 is invested in real estate that returns $1 million after 47 years, the tyranny of compounding costs takes away roughly $750,000 of the return and leaves the real estate investor with only $250,000 of the gain. In contrast, if $150,000 is invested in an S&P 500 index fund that returns $16 million after 47 years, the low cost index fund takes away very little of the return and leaves the stock market investor with nearly $16 million.

Finally, perhaps the most important fact overlooked by many homeowners is that the increase in the value of their home cannot be used as a future income stream because the only way to do that would be to use a home equity loan or line of credit, which is the worst possible thing a homeowner can do. In fact, a personal residence is not a financial investment because a home does not provide spendable income from price appreciation.

Instead, the purpose of home ownership is not purely financial but is primarily psychological — a home should provide good family memories over the years and peace of mind when the mortgage is paid off. In comparison, the purpose of a low cost S&P 500 index fund is purely financial — the S&P 500 should increase in value faster than inflation and home prices to provide ample spendable income in 20+ years.

It’s great the kids bought their first home sweet home and are next planning to invest in the stock market. My unique perspective is that home ownership and stock investing are both very important things for nieces and nephews to do — buy a home as a nice place to live comfortably and then follow Uncle Warren’s expert advice to buy low cost stock index funds like SWPPX that has an expense ratio under 0.05% and forget about it for 20+ years.

At that point 20+ years from now, having a paid off home with a lifetime of precious memories and having low cost stock index funds that provide a good income stream would be a great situation for nieces and nephews to be in!

BLOG POST 10 — Ask Uncle Alvin About His Unique Perspective on Roth IRAs and Backdoor Roths

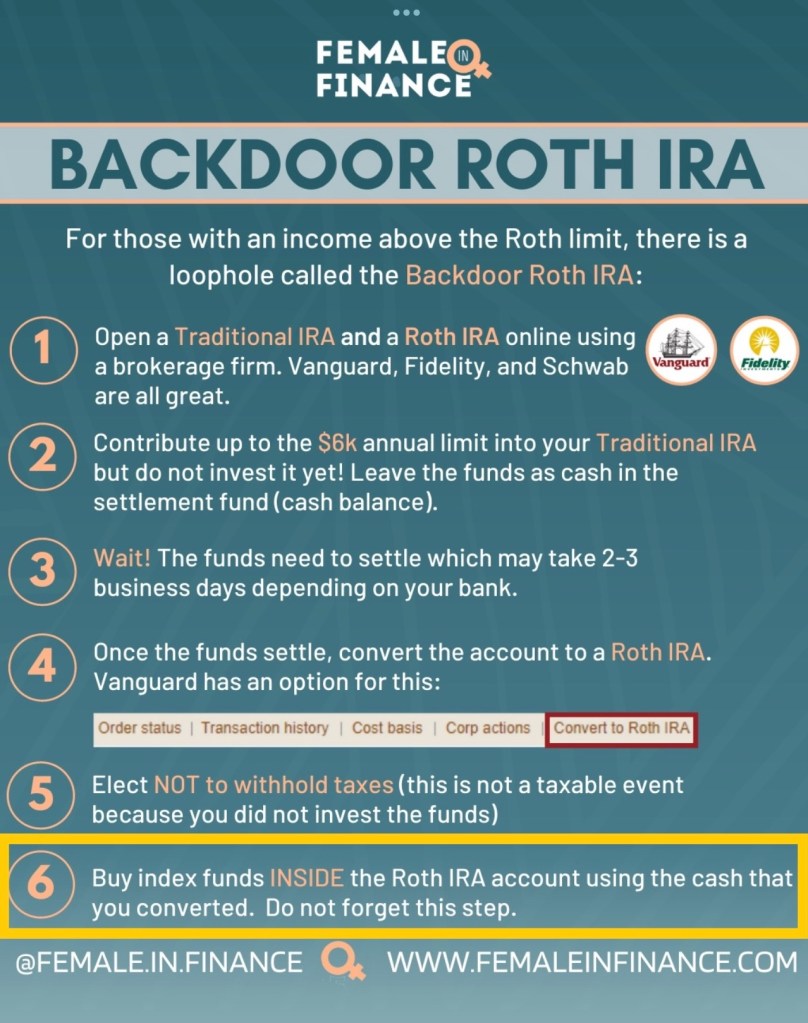

Can Uncle Alvin talk about how to do a Backdoor Roth?

Uncle Alvin’s unique perspective is that Roth IRA accounts are one of the best investment accounts ever for nieces and nephews. Unlike a traditional IRA and 401k account where the contributions are not taxed but the distributions are taxed as ordinary income and there is a requirement to take money out of the account after age 73, in a Roth IRA the contributions are taxed but the distributions are completely tax-free and there is no requirement to take money out of the account.

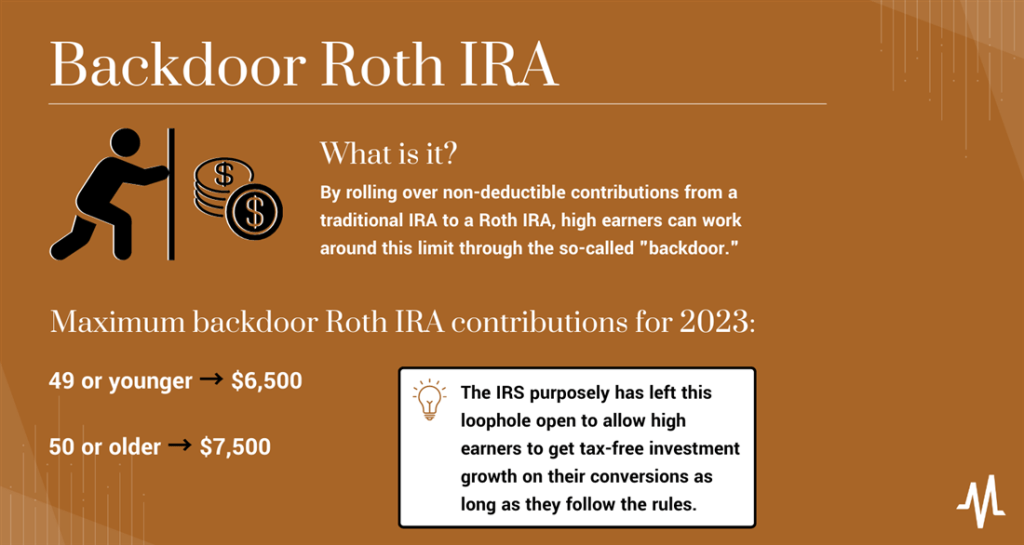

However, unlike a traditional IRA or 401k, the Roth IRA is supposed to be available only to nieces and nephews who receive taxable compensation that is under certain annual income limits. However, nieces and nephews who receive compensation that is higher than those limits can still establish a Roth IRA every year by using what is known as a Backdoor Roth IRA, which involves opening a traditional IRA with after-tax (non-deductible) funds and then rolling it over almost immediately (typically within a week) to a Roth IRA.

In other words, nieces and nephews who cannot directly open a Roth IRA in any given year because their compensation exceeds the income limits, can still indirectly establish a Roth IRA through a “backdoor,” and the easiest way to do that is to call Uncle Schwab (or any brokerage firm like Uncle Fidelity and Uncle Vanguard) and simply ask their friendly Roth IRA specialists to do a Backdoor Roth for that year.

For more information, here are articles from Uncle Schwab and Uncle CNBC about the Backdoor Roth.

For nieces and nephews who can max out the 401k and Roth IRA contributions every year and are interested in investing even more for retirement — there is a Mega Backdoor Roth that involves contributing to both a traditional 401k and a Roth 401k, as well as a Backdoor Roth. For more information, here is an article from Uncle Fidelity about the Mega Backdoor Roth.

However, while everyone can contact their friendly brokerage firm like Charles Schwab or Fidelity and have them handle the simple and routine process of establishing a Backdoor Roth, nieces and nephews who are interested in the Mega Backdoor Roth would need to contact their friendly 401k provider and ask how to proceed because the Roth 401k is relatively new so not all 401k plans offer it, and not everyone is eligible, and it is a more complicated process.

VERY IMPORTANT NOTE: This may seem obvious but Uncle Alvin has seen this happen before — when nieces and nephews open any investment accounts and put money into those accounts, it is very important to do STEP 6 as outlined below and invest themoney in the accounts by buying low cost index funds with expense ratios less than 0.05%!

BLOG POST 9 — A Nephew Asks For Uncle Alvin’s Unique Perspective on 401k Investment Options

Starting this month, we have access to the 401k plan through my employer, with some kind of employer match as well. We get to choose the investment that these funds go toward, so we wanted to get your perspective on which of these options might be good for us. The default is to go into the 2055 target date fund. I was thinking the S&P 500 Index fund might be a good option given its low expense ratio and good history. Let us know what you think – we are subscribing to the Uncle Alvin plan!

Great that you have access to the 401k plan in the new year! Very happy to provide my unique perspectives on investing based on personal experience and the wise perspectives of the greatest investors of all time like Uncle Warren and Uncle Bogle.

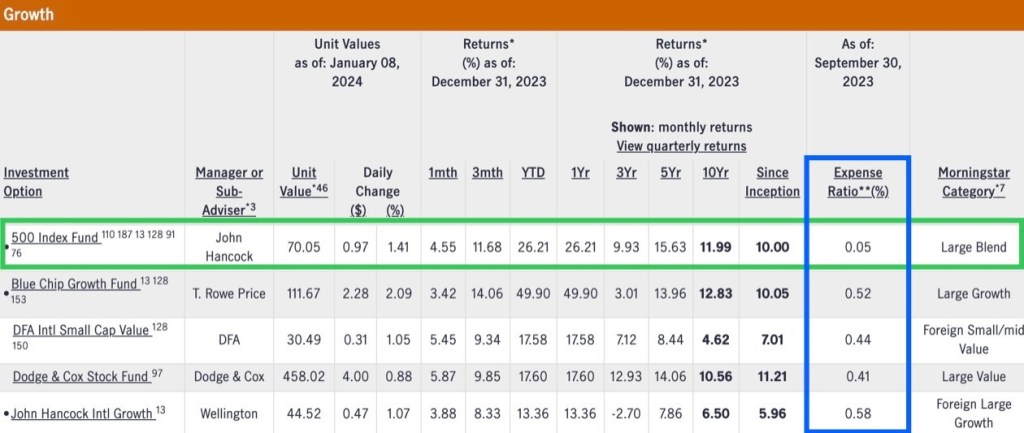

There are many investment options in your 401k plan to choose from. However, if you know about Uncle Warren’s perspective that the best thing investors can do is to put 90% of their money into a low cost S&P 500 index fund (see BLOG POST 1), and you know about Uncle Bogle’s perspective on the tyranny of compounding costs (see BLOG POST 2), then the best option out of all the investment options is the S&P 500 Index Fund that has an expense ratio of 0.05%.

I looked at the other investment options and their expense ratios are generally around 0.5%, which means the other investment options are about 10 times more expensive than the S&P 500 index fund, and high expenses are bad for investment accounts. Regarding the default choice being target funds, Uncle Warren says investors are better off with 90% in S&P 500 index funds and don’t need more than 10% in bonds, but target funds typically increase over time to 60% in bonds, which means investors in target funds unfortunately can have 6 times more in bonds than Uncle Warren recommends.

Fortunately, your 401k offers a low cost S&P 500 index fund, and Uncle Alvin agrees with Uncle Warren that S&P 500 index funds are the best 401k investment option for nieces and nephews of all ages. Always fun to answer any questions about my favorite subject any time. Happy to provide my perspective and you can ask others for their perspectives, and then use your good judgment to decide what is best for your fam!

BLOG POST8 — A Niece Asks For Uncle Alvin’s Unique Perspective On Her Friend’s Stock Investment: What Would Uncle Elon Musk Do?

Uncle Alvin recently met up with a fellow uncle and his family in Lisbon, Portugal. His daughter said her friend recently bought a stock and was very nervous about it, checking the price every hour and eventually selling it for a loss of around 10%. Could her friend have done anything differently?

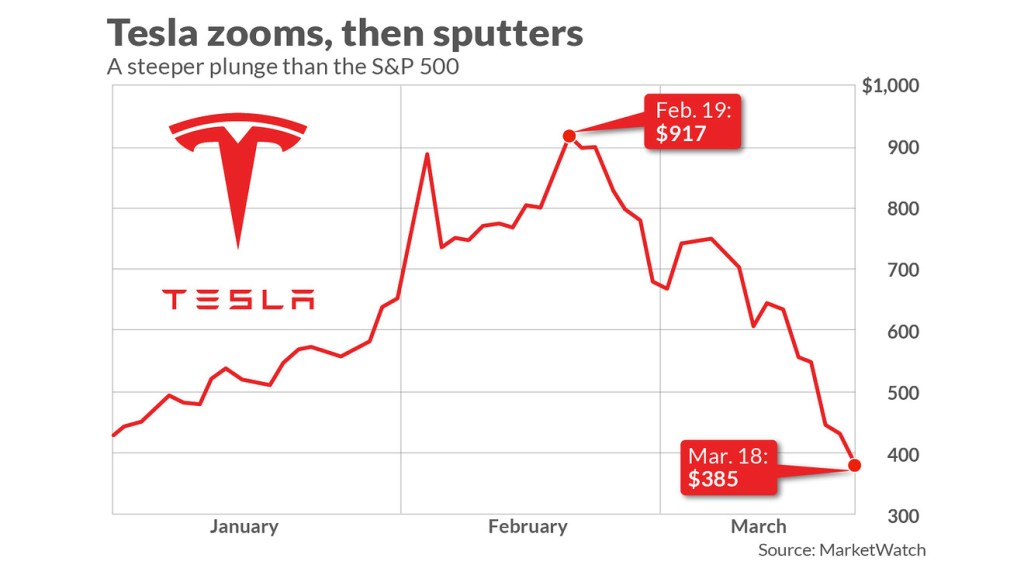

We don’t know what stock the friend bought, but let’s assume the friend did his best investment research and bought Tesla, one of the greatest stocks of all time, which made Uncle Elon the richest person in the world and would have been a great investment for the friend.

Assuming that is the case, then my unique perspective is that the best thing nieces and nephews and their friends can do after buying the stock, is to do what Uncle Elon did with his Tesla stock — even if it drops 10% or 25% or 50% or more — forget about it and do nothing but hold it. However, that sounds easy enough in theory but is very difficult to do in real life.

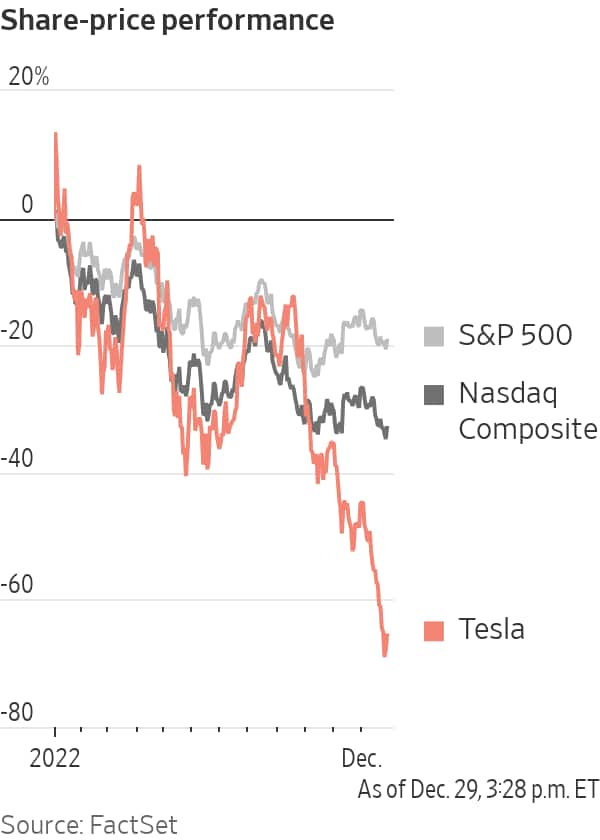

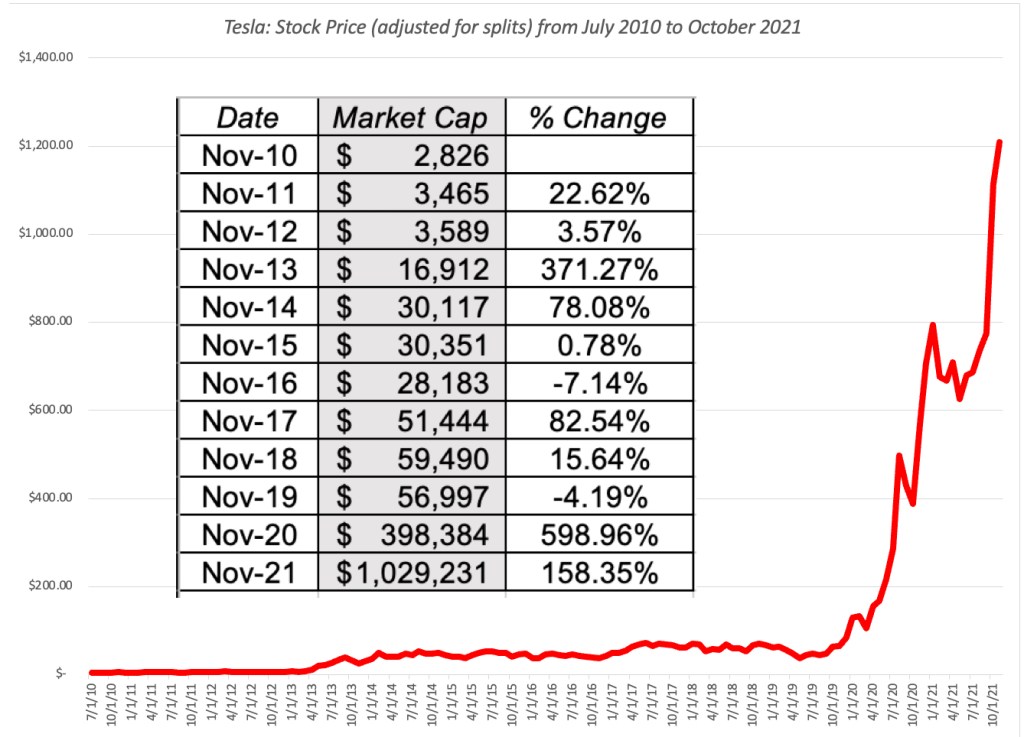

Psychologically, the difficult thing to do is that holding Tesla stock as it progressed through a seemingly endless series of 10% and 25% and 50% and 75% drawdowns on the way to consumer acceptance of electric cars and being one of the most valuable companies in the world, would have been too stressful and depressing for most investors — yet holding Tesla stock through all the declines is exactly what Uncle Elon did. For example, in the spring of 2020, Tesla fell not just 10%, but fell an astonishing 60% in just one month.

Then in 2022, Tesla fell 75% in one year.

Yet even including these unbelievably swift and severe drops, Tesla increased 10X and then another 10X and many more times since its IPO, and by simply holding Tesla stock instead of trying to market time Tesla stock, Uncle Elon became the richest man in the world.

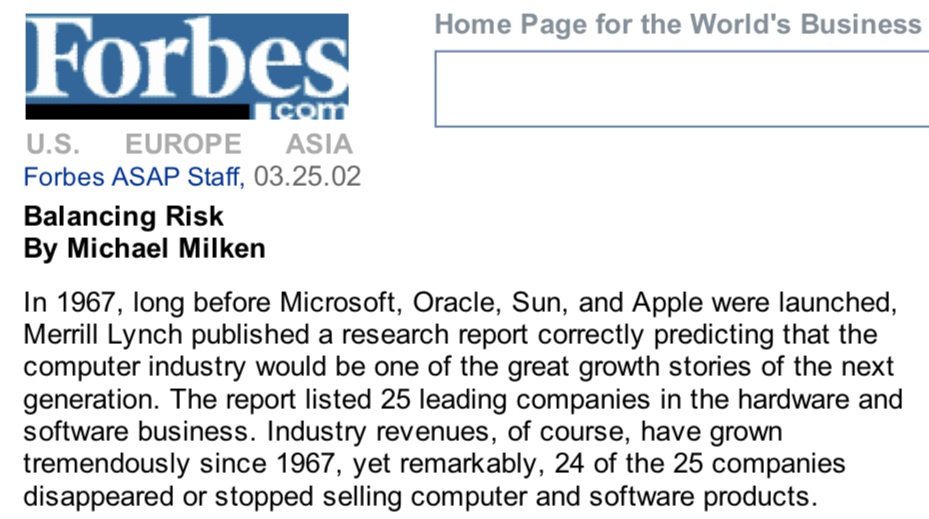

Objectively, another difficult thing to do is that the statistical odds of picking stocks that turn out to beat the market are very low for most investors. Even very knowledgeable and experienced stock pickers who do their best possible research are still much more likely to pick the many stocks that ultimately turn out to disappoint or become worthless like Enron or Lehman, instead of the handful of stocks that turn out to be great like Tesla, as Uncle Michael Milken explains below:

Investors can do their best research to try to pick stocks that beat the market, yet as Uncle Milken observes, even professional investors with access to the best investment research are much more likely to pick stocks that disappoint or disappear, and even if investors pick stocks that actually turn out to be good in the long run, it might be very difficult to hold through the inevitable depressing drawdowns when it seems the stocks might turn out to be like the many stock picks that were once stars but then disappeared, like Enron.

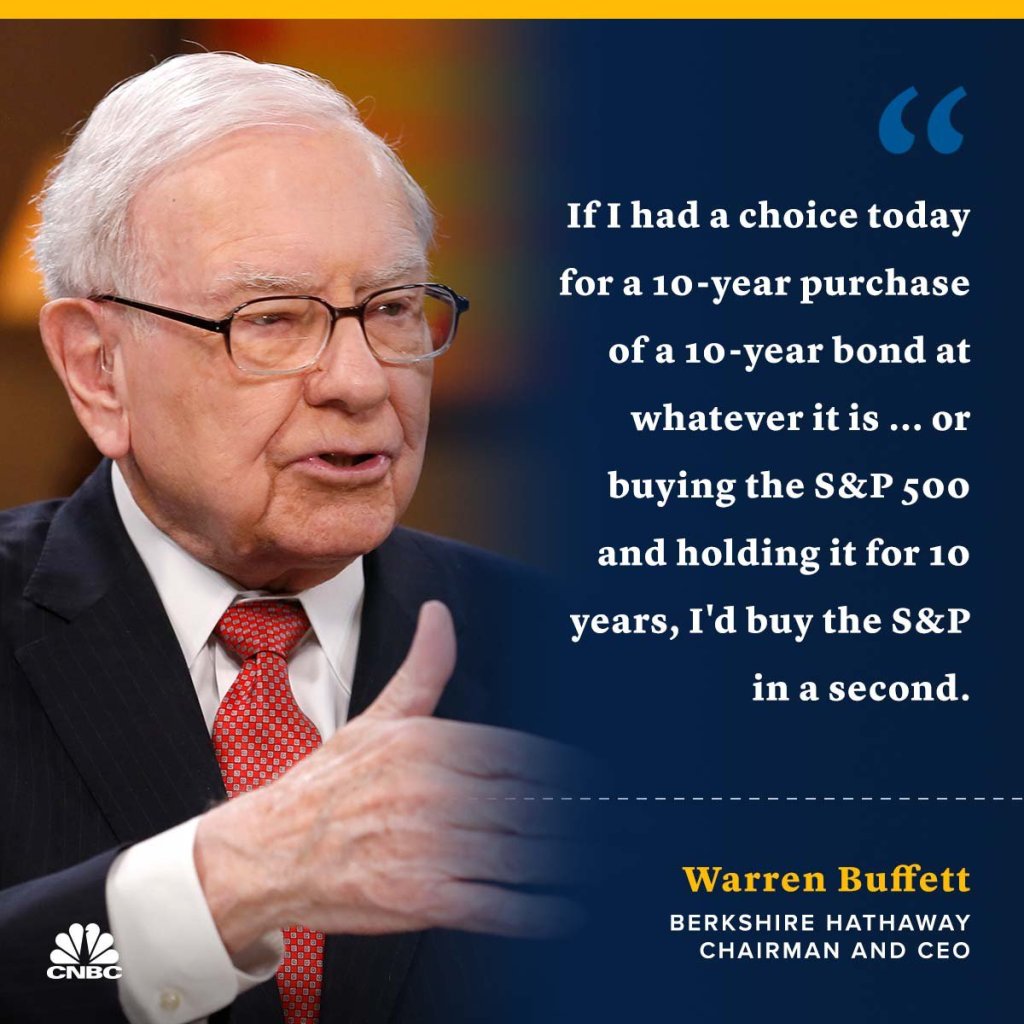

Therefore, as Uncle Warren recommends, the best thing nieces and nephews and their friends can do is to use 90% of their life savings to buy low cost S&P 500 index funds with expense ratios less than 0.05%, because index funds have never become worthless but have always turned out to make money and beat the vast majority of investors in every 20+ year holding period since the inception of the S&P 500.

In summary, by following Uncle Warren’s advice and using life savings in tax-deferred retirement accounts such as 401k and IRA accounts to buy and hold index funds, nieces and nephews and friends can stress less and build wealth faster than the vast majority of investors by avoiding common investment mistakes like stock picking and market timing.

In addition, risk-tolerant nieces and nephews with an avid interest in investing can use risk capital in taxable investment accounts outside of their retirement accounts to try to build wealth faster than index funds, knowing in advance there is a lifelong learning curve and difficult psychological and objective hurdles to beating the market.

BLOG POST 7 — A Niece Asks For Uncle Alvin’s Unique Reaction To A Little Nephew’s TikTok Video

It would be cool if you did a reaction to this video!

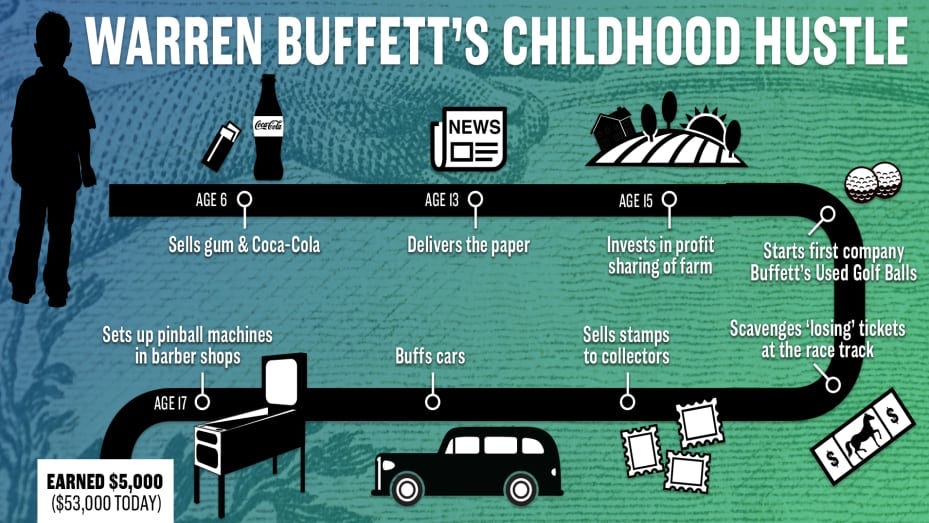

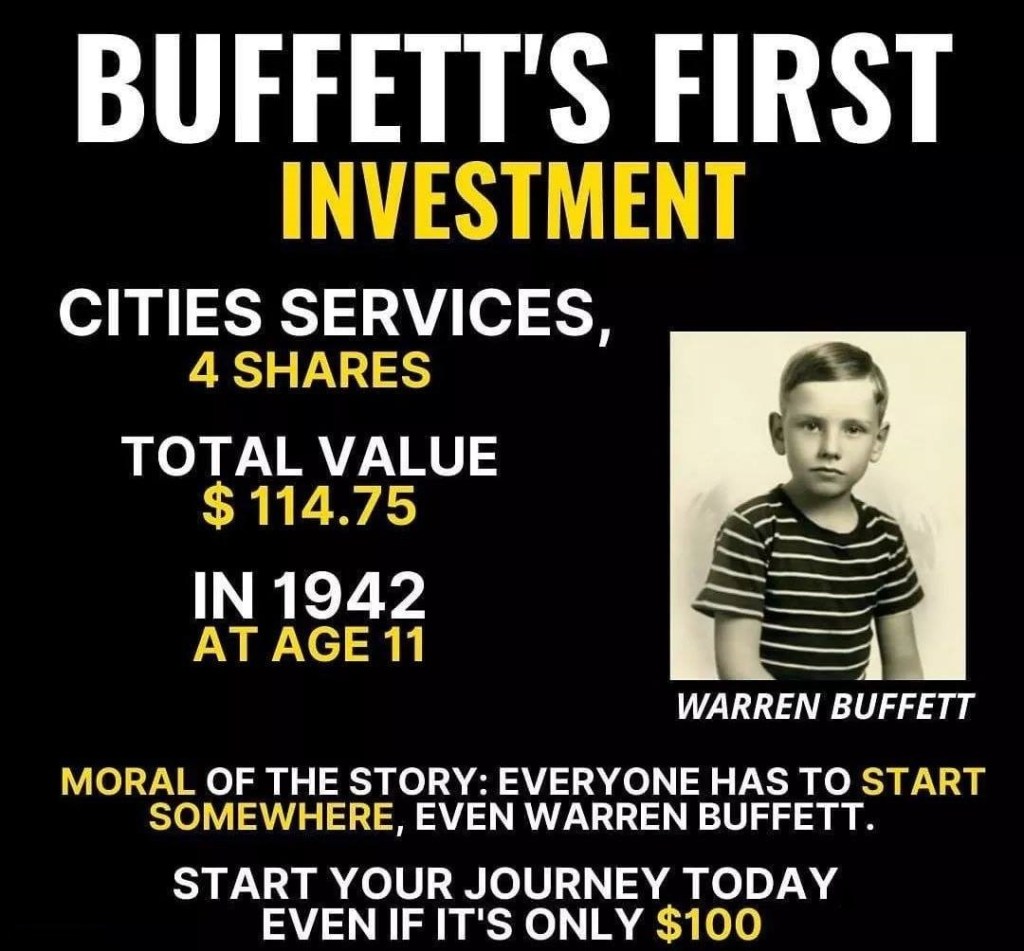

This little nephew wants to do exactly what Uncle Warren Buffett did when he was a kid — little Warren saved all his gift money and all the money he made from his childhood jobs selling bubblegum, soda and newspapers.

Little Warren not only saved, but most importantly, he investedwhat he saved by making his first of many stock market investments when he was only 11 years old.

So if nieces and nephews want to start following in the footsteps of Uncle Warren, Uncle Alvin says that:

1) the first step is to follow the good example of this little nephew and save.

2) the second step is to follow Uncle Warren’s good advice and invest in low cost stock index funds with expense ratios less than 0.05%.

3) an optional third step after maxing out the tax-deferred retirement accounts in low cost stock index funds, is to become knowledgeable about investments and allocate a portion of taxable investment accounts to risk capital for investing in riskier assets.

BLOG POST 6 — A Nephew Asks For Uncle Alvin’s Unique Perspective on Risk Capital and FOMO

I really appreciate your objective analysis and the opportunities/risks they offer for us. However, to borrow a term from the youths, using only 10% of net worth for risk capital gives me massive FOMO when I do accidentally hit NBA-level alpha gains. Ultimately, I realize that proper investor discipline is still the copacetic path.

Thanks for the kind comments! Uncle Alvin knows that nieces and nephews may find it fun and educational to try to hit NBA-level alpha gains and might have FOMO if they do not try to beat the S&P 500, because aunts and uncles including Uncle Alvin also enjoy trying to maximize alpha and learning more along the way.

My unique perspective on FOMO is that investing is not only objective and analytical — investing is also psychological. Rationally, investors should follow Uncle Warren’s objectively good advice and put their investments into very low cost S&P 500 index funds, with no FOMO.

Psychologically, risk-tolerant nieces and nephews who follow Uncle Warren’s advice but enjoy investing like Jeremy Lin enjoys basketball, might have big-time FOMO because they feel they don’t have enough in riskier assets and strategies to have a chance of getting into the NBA.

One unique and practical perspective that Uncle Alvin followed, and risk-tolerant nieces and nephews can also follow to minimize FOMO, is:

1) first, before doing anything else, max out the tax-deferred retirement accounts (401Ks, Roth and traditional IRAs, etc.) into low cost stock index funds with expense ratios less than 0.05%.

2) then allocate a portion of taxable investment accounts as risk capital for riskier assets and have fun working on a track record that can be good enough to get into the NBA!

BLOG POST 5 — A Nephew Asks For Uncle Alvin’s Unique Perspective on Higher Risk Strategies to Maximize Returns

1) If the goal of investing is to build wealth, shouldn’t we be moving money to maximize the return?

2) How much of our net worth do you think we can allow to do high risk trades to maximize alpha?

For question 1), I agree the goal of investing is to build wealth. There is a popular perspective that buying a low cost stock index fund is “too slow” and “too boring” to build wealth, but my unique perspective is that nieces and nephews can build wealth faster than most investors by simply buying and holding a low cost S&P 500 index fund, because the S&P 500 builds wealth faster than 80% of all funds!

As for moving money to try to maximize the return, I would defer to Uncle Warren who says the best thing investors can do is to simply put their money in an S&P 500 index fund with an expense ratio less than 0.05%, meaning buy and don’t move money, or as Uncle Depp and Uncle Pacino would say, just buy and —

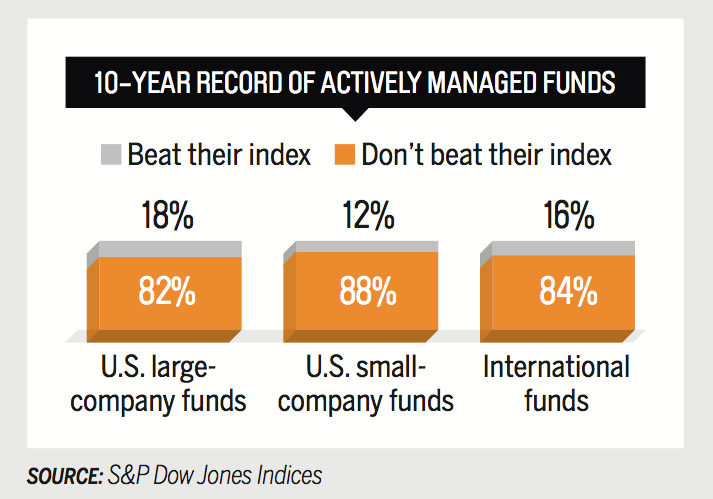

In theory, moving money may maximize return, but in practice, moving money is more likely to minimize return. For example, Uncle Bogle found that more than 80% of fund managers who actively move money around to try to beat an index like the S&P 500, don’t beat their index. Unfortunately, this means that more than 80% of investors who move money around to try to beat the market, don’t beat the market. In other words, for the vast majority of investors, moving money actually minimizes return.

For question 2), Uncle Warren recommends that investors put 90% of their money into an S&P 500 index fund and 10% into a bond fund. You seem to be a risk-tolerant nephew with an avid interest in learning more about investing, so my unique perspective is that instead of moving 10% of your money into a bond fund, you can consider modifying Uncle Warren’s recommended portfolio by moving 10% into higher risk assets and trading strategies to try to maximize alpha, because you can definitely learn more about investments by trying to maximize alpha with risk capital than being in a bond fund!

However, the number of people who can maximize alpha is probably like the number of people who can play in the NBA — a very small number. Everyone tries to generate alpha so it can be very tough to maximize alpha, but it might be very educational for you to consider the portfolio below that allows the use of risk capital to try to generate alpha with the dream of getting into the NBA one day, while limiting maximum losses to a small percentage of net worth and treating losses (inevitable along the way) as the cost of tuition in the learning process:

Uncle Warren’s Modified Portfolio For Risk-Tolerant Investors: 90% in low risk S&P 500 index funds and 10% in risk capital.

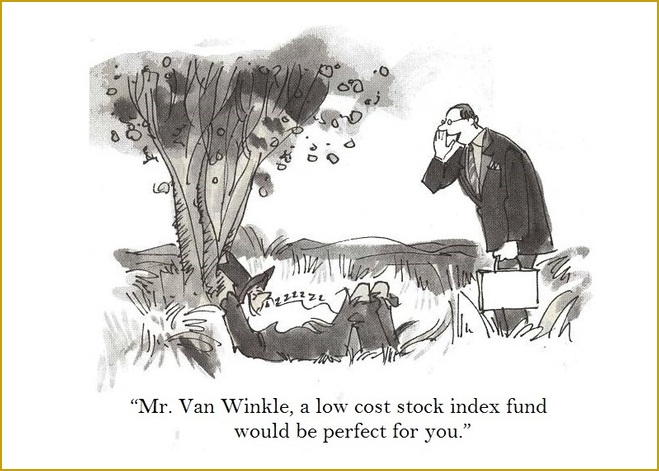

BLOG POST 4 — Ask Uncle Alvin About Uncle Rip Van Winkle’s UniquePerspective On How Long To … Fuhgedaboudit

Uncle Fidelity showed that investors who forgot about their investments, did the best. Of course, investors don’t want to completely … fuhgedaboudit, because they want to eventually benefit from their investments. So nieces and nephews may ask Uncle Alvin, as a practical matter, how long should they … fuhgedaboudit?

I now want to tell nieces and nephews about Uncle Rip Van Winkle’s perspective on sleeping for 20 years applies to investing. As you can see from this article, What if Rip Van Winkle Invested in the U.S. Stock Market, there were many unexpected events and scary declines during every 20-year period for the U.S. stock markets, but investors who bought low cost stock index funds and did nothing else and just forgot about it for 20 years, always made money and did the best.

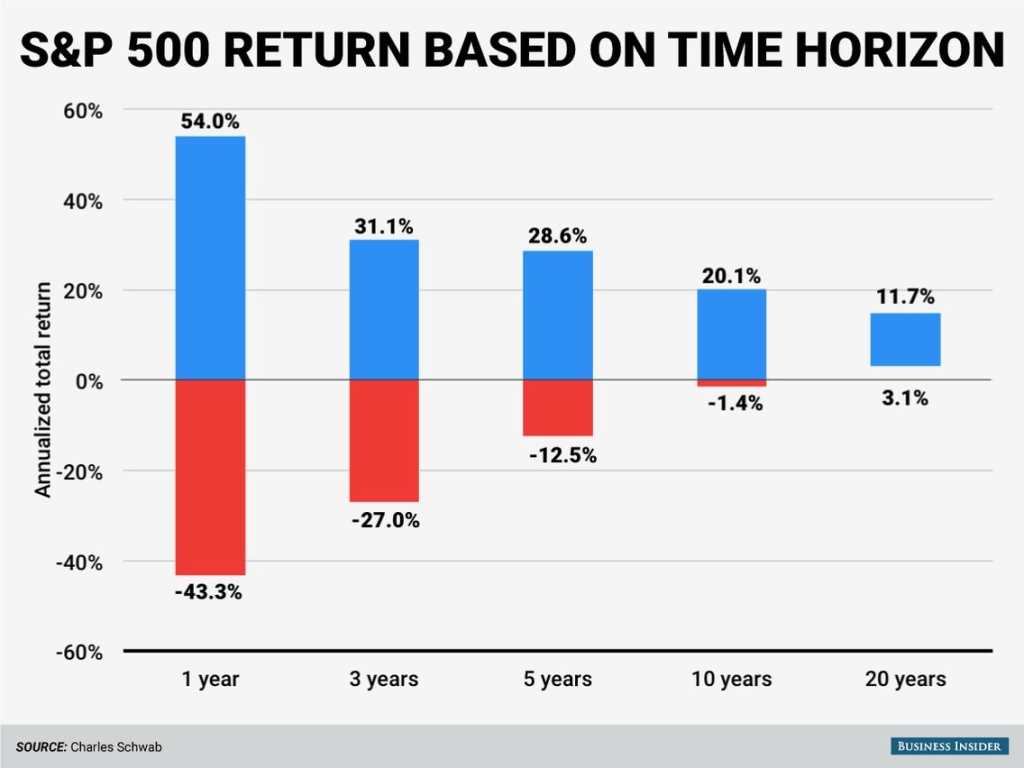

Stock markets are risky in the short-term, as investors saw in 2022 when the S&P 500 index fell into a bear market, but the risks recede and the rewards emerge in the long-term. In other words, investors who buy low cost stock index funds can experience significant risks and do poorly after 1 year or 3 years or 5 years or even 10 years.

However, nieces and nephews who buy low cost stock index funds like Schwab’s S&P 500 index fund with an expense ratio under 0.05% (symbol SWPPX) and forget about it for 20+ years, can reap the rewards and make money in every 20-year period in history despite the unexpected surprises and scary markets that always happen along the way.

BLOG POST 3 — Ask Uncle Alvin About Uncle Fidelity’s Unique Perspective On Which Investors Did Best and — Forget About It

For most activities that nieces and nephews like to do, such as art or music or sports, the more you do, the better you do. For example, the more you practice painting and guitar and basketball, the better you do in those activities.

However for investing, the less you do, the better you do!

An example of this is a study that one of the largest fund companies in the world made — Fidelity Reviewed Which Investors Did Best And What They Found Was Hilarious — that showed Fidelity’s best-performing accounts were actually accounts where their customers bought Fidelity funds and then completely forgot about their accounts. In other words, the less that investors did, the better they did. In fact, when Fidelity’s investors forgot about it and did nothing more, they did the best.

So if nieces and nephews ask what are the secrets to a meaningful life and successful investing, Uncle Alvin says three of the secrets are to:

1) work hard and have fun doing the things you like,

2) be helpful to others, and

3) get into the habit of putting part of birthday and holiday gifts and part-time and full-time jobs in an investment account at say Schwab and a retirement account at work, and regularly buy low cost stock index funds with expense ratios less than 0.05% like SWPPX —

Then after buying low cost stock index funds, just do what Uncle Johnny Depp and Uncle Al Pacino would say —

BLOG POST 2 — Ask Uncle Alvin About Uncle Jack Bogle’s Unique Perspective On The Tyranny of Compounding Costs

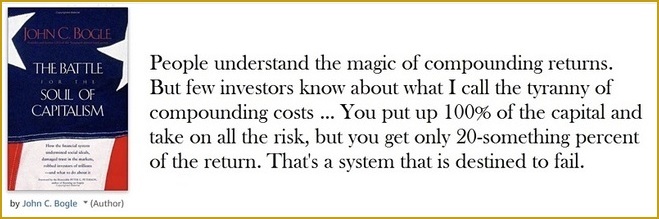

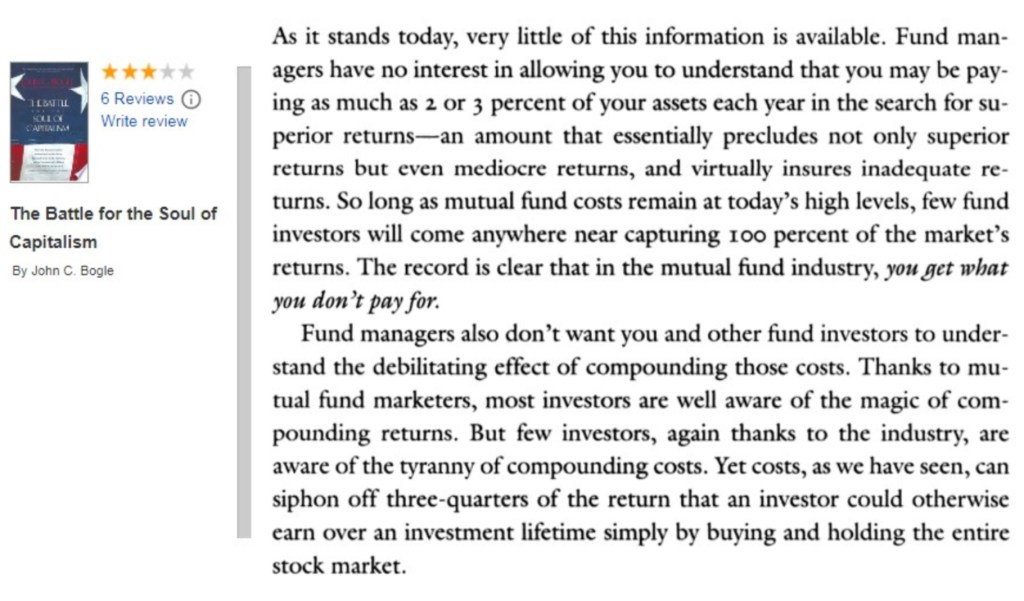

Nieces and nephews may also ask Uncle Alvin, what is the worst thing that investors can do so they can avoid making the same mistake? One of the worst things investors can do is buy high cost stock funds because these types of funds take away 75% of the investment gains from unsuspecting investors.

Uncle Jack Bogle, the founder of the Vanguard Group and an investment expert who introduced the first low cost stock index fund to investors, explains the disadvantages of high cost stock funds and the advantages of low cost stock index funds.

In his book The Battle for the Soul of Capitalism, Uncle Bogle explains that high cost stock funds are scams that are destined to fail because the tyranny of compounding costs can take away roughly 75% of the market’s return and leave investors with only about 25% of the market’s gains.

Many investors ignore the fees and hidden costs charged by high cost stock funds because 1) the annual fees of 1% or higher might not seem like a big deal and may even seem too “small” to ever worry about, and 2) the fees and costs are never itemized but buried in the fine print and silently taken out without any further notice to investors.

This means that high cost stock funds become toxic assets over time because unwary investors don’t realize most of the return has been taken away by the tyranny of compounding costs until it’s too late, after too many years have passed.

For example, if the return from the stock market after decades of investing is $1 million dollars, a high cost mutual fund would take away as much as $750,000 dollars and leave an investor with only $250,000, compared to a low cost stock index fund with an expense ratio under 0.05% that would leave an investor with nearly the entire $1 million.

To the contrary, the investment industry has a vested interest in keeping investors in the dark about fees, so bad investments like high cost stock funds can walk away with 75% of the market’s gains after decades of investing.

Fortunately, Uncle Alvin’s nieces and nephews who are reading this blog are no longer in the dark about fees and are now aware of the tyranny of compounding costs, so they can cut high cost stock funds out of their portfolios that leave investors with only 25% of the return.

Nieces and nephews can put much better investments into their portfolios, like low cost stock index funds with expense ratios under 0.05% that leave investors with nearly 100% of the return.

So Uncle Alvin says that one of the best things nieces and nephews can do to get started and stay on the road to great investment outcomes is:

1) follow Uncle Bogle’s expert investment advice to avoid high cost stock funds because these funds leave investors with as little as 25% of the market’s return, and —

2) follow Uncle Warren’s expert investment advice to just buy low cost stock index funds that leave nieces and nephews with nearly 100% of the return and — forget about it.

BLOG POST 1 — Ask Uncle Alvin About Uncle Warren Buffett’s Unique Perspective on Investing

Nieces and nephews may ask Uncle Alvin, what is the best thing that investors can do? One of the best investors in the world, Uncle Warren Buffett, says the best thing to do is buy a very low cost S&P 500 index fund.

So Uncle Alvin says the best and easiest thing that nieces and nephews can do to invest is to just follow Uncle Warren’s expert investment advice — buy low cost stock index funds with expense ratios less than 0.05% like SWPPX and do nothing more.

BLOG POST 3 — Ask Uncle Alvin About Uncle Fidelity’s Unique Perspective On Which Investors Did Best and — Forget About It